EIQ - who are they working with?

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 3,084,000 EIQ Shares and the Company’s staff own 112,000 EIQ shares at the time of publishing this article. The Company has been engaged by EIQ to share our commentary on the progress of our Investment in EIQ over time.

Our tech Investment Echo IQ (ASX:EIQ) has an AI-powered algorithm that helps detect heart diseases.

Diseases like heart failure and aortic stenosis.

Aortic stenosis is a disease where the heart’s aortic valve is narrowed and doesn’t open fully. This restricts blood flow to the rest of the body - it can be fatal if left untreated.

(remember this definition - it's important for later)

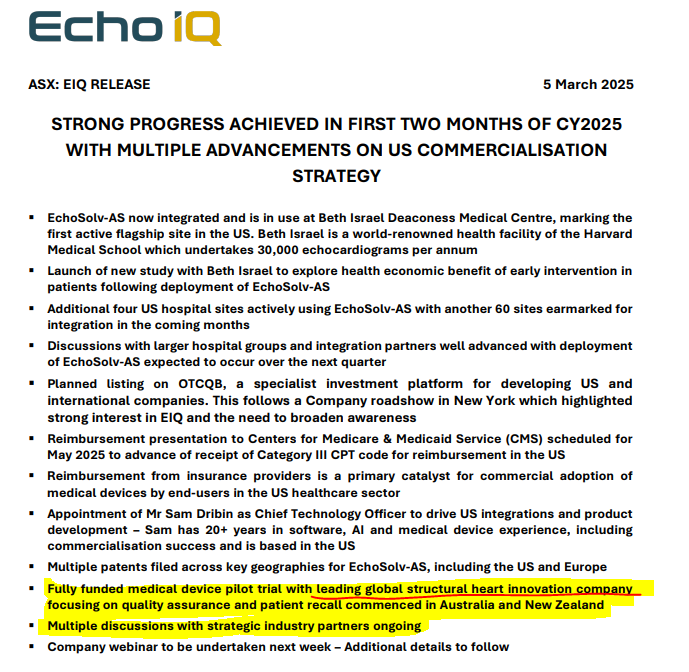

Yesterday EIQ released a comprehensive update on all aspects of the business, five months after getting US FDA clearance for helping cardiologists detect a heart disease called aortic stenosis.

With US FDA clearance in hand, EIQ has quickly started commercialisation - it’s hired an experienced US based CEO, secured a reimbursement code (important for how EIQ makes money), and integrated its tech in five US hospitals.

The new US based CEO is 2 months into the job and tasked with revenue growth in the US. He has been very busy - check out the list in the image below.

If you don't want to read the below, you can hear from him directly next week in a webinar covering EIQ’s commercial plans, which you can register for below. The company is also running a Q&A session for investors.

Click here to register for EIQ’s Webinar

(Source - 5/03/2025 EIQ announcement)

A few things in this list stood out to us...

We will unpack EIQ’s list of achievements in today’s note, but something toward the end really caught our eye.

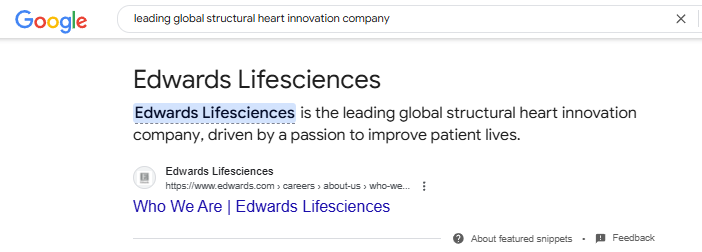

EIQ mentioned it is conducting a fully funded device pilot trial with a “leading global structural heart innovation company”.

Sounds interesting... who could that be?

A quick Google search for “leading global structural heart innovation company” comes up with $42BN capped Edward Lifesciences:

(Of course, EIQ has not identified their partner and the commentary below is complete speculation on our part - there’s many global companies working in the heart space)

Following our Google search, we listened in to Edwards LifeSciences Feb 11th earnings call (listen to that call here or read the transcript here)

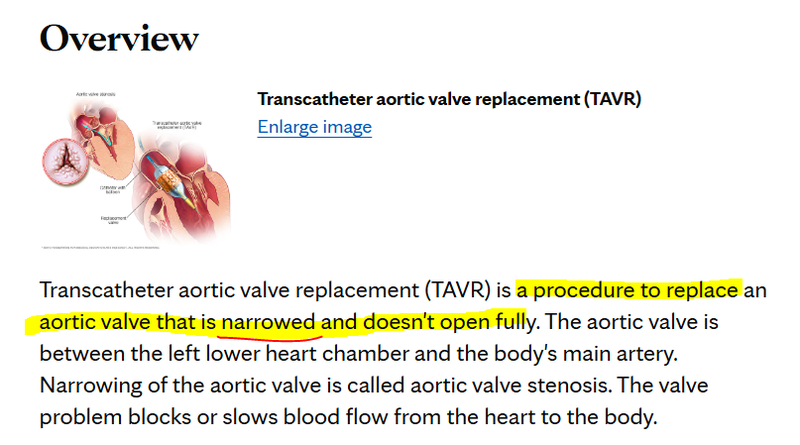

The CEO of $42BN Edwards is excited about an "important growth driver” in their TAVR product (Transcatheter Aortic Valve Replacement)

Their TAVR product replaces a “heart valve that is narrowed and doesn’t fully open”:

Here’s where EIQ’s technology could come in:

EIQ’s technology DETECTS where the heart's aortic valve is narrowed and doesn’t open fully.

Edwards lifeSciences tech TREATS THE PROBLEM where the heart's aortic valve is narrowed and doesn’t open fully.

EIQ has already demonstrated that with its tech it can produce a 72% increase in detection vs human-only diagnosis for severe aortic stenosis.

We think more accurate and earlier detection of patients would be of great interest to the $42BN Edwards LifeSciences...

In the earnings call the Edwards Lifesciences CEO said “Clearly, indication is a big thing. Once it's on label, that certainly is helpful because it gives us ability to promote directly where until that happens, we're not allowed to promote directly.”

In medicine, an “indication” means a sign, symptom, or medical condition (like the ones EIQ helps detect) that leads to the recommendation of a treatment, test, or procedure.

Edwards LifeSciences has recently been active on the M&A front

Recently, Edward’s LifeSciences acquired two companies for a combined US$1.2BN (contingent on FDA approvals - one of which was JenaValve Technology).

JenaValve is currently developing a TAVR (transcatheter aortic valve replacement) therapeutic product, which it expects to receive FDA approval for in 2025.

(Source)

So, Edwards is paying almost A$2BN for a medical device that can treat aortic stenosis...

EIQ’s technology can help detect aortic stenosis more accurately, with more diagnoses, it means a company with a therapeutic product could treat more patients - increasing its addressable market, and improving health outcomes at the same time.

I.e. improved or earlier detections and diagnoses could potentially open up a whole new segment of previously undiagnosed patients that will benefit from Edward Lifesciences’ product.

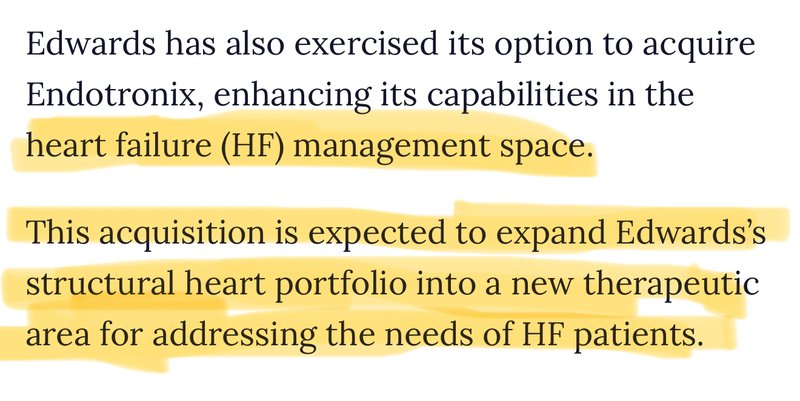

The second part of the Edwards M&A deal was the acquisition of Endotronix.

Endotronix is Edward’s way of “enhancing its capabilities in the Heart Failure management space”.

(Source)

Disclaimer: all of this commentary is complete speculation on our part as EIQ Investors based on Google searches and connecting dots (that may not even exist) from the Edward’s Life Sciences earnings call - read the full transcript here and do a search for “TAVR”.

EIQ is a high risk pre revenue small cap stock, and successful investing outcomes are no guarantee.

REMINDER: EIQ is working on AI tech that could enhance Heart Failure detection and diagnosis rates too.

Heart disease is the leading cause of deaths in adults, and Heart Failure costs the US healthcare system approximately $60 billion annually.

FDA clearance for EIQ’s Heart Failure tech is expected later this year... and that market opportunity is ~10x bigger than aortic stenosis for EIQ.

A US$42BN company paying billions of dollars for therapeutics is a good signal that Big Pharma would see a lot of value in companies that can help with diagnosis (and drive more treatment).

We think large medical device companies and Big Pharma will likely be very interested in the high growth, high margin Software as a Service (SaaS)-style returns of companies with the tech to make it happen.

That’s because there will be more patients that were previously undiagnosed that can now get the treatment they need.

That is where we think the big opportunity lies for our AI-based healthcare company EIQ.

EIQ uses AI-driven technology and proprietary software to improve decision making in cardiology.

After years of developing its technology, plus moving along the regulatory and commercialisation pathway, EIQ is getting very close to turning on the revenue tap.

Next Thursday, 13th March, EIQ’s CEO will provide a progress update on the US commercialisation strategy for EchoSolv-AS over the first two months of CY2025, along with an outlook on the Company’s clinical development pipeline and other opportunities.

Click here to register for EIQ’s Webinar

Heart disease is the leading cause of deaths in adults.

Last year, EIQ secured FDA clearance for an AI tool that can be used by cardiologists to help detect a specific heart disease - aortic stenosis.

Aortic stenosis is a heart valve condition that costs the US healthcare system more than ~US$10BN each year.

1.2 million people are diagnosed (by cardiologists) with aortic stenosis, with an additional 1.5 million ‘mild to moderate’ diagnoses.

EIQ has already integrated its technology for aortic stenosis into a top US-based hospital network and it has 60 more hospitals in its pipeline.

The company also hired a new US based CEO, Dustin Haines to drive EIQ’s commercial strategy and growth in the US. He officially started in January.

Earlier this week we got a comprehensive update on the first few months of the new CEO’s tenure - that long list you saw above.

Here is a quick summary as to what EIQ has been doing over the last two months:

- Integration at Beth Israel Deaconess Medical Center - Beth Israel is a prestigious Harvard Medical School facility that performs 30,000 echocardiograms annually. This is validation of EIQ’s tech and an initial “beach head” for EIQ to build revenue from.

- Four additional US hospital sites are actively using EchoSolv-AS - with plans to integrate the technology at 60 more sites in the coming months. More deals will mean more revenue to EIQ.

- Reimbursement strategy advancing - EIQ will present to the Centers for Medicare & Medicaid Service (CMS) in May 2025. Reimbursement codes are central to how EIQ will get paid for its services.

- Chief Technology Officer (CTO) appointed - Sam Dribin has been appointed to drive US integrations and product development. Sam is an expert at AI healthcare tech roll-outs.

- US listing process underway (OTCQB) - Echo IQ plans to list in the US to broaden its exposure to US investors.

- The BIG one: “Multiple discussions with strategic industry partners ongoing” - we’re very interested to hear more on this aspect of EIQ’s commercialisation strategy as any potential licensing or partnership deal could help underpin another sustained re-rate for the company.

We’ve got our detailed breakdown of what these key points from EIQ’s latest update mean further down.

Next Thursday, 13th March, EIQ’s CEO will provide a progress update on the US commercialisation strategy for EchoSolv-AS over the first two months of CY2025, along with an outlook on the Company’s clinical development pipeline and other opportunities.

Click here to register for EIQ’s Webinar

We’ll be watching.

We think all of the above developments demonstrate that EIQ is doing a good job of executing its US market entry strategy.

We think there is hugepotential for EIQ to quickly grow market share in the US too - there are over 6 million echoes performed in the US annually.

Which is why the upcoming meeting with the reimbursement code regulators (the CMS from above list) in the US is such an important catalyst for EIQ.

(This important regulatory meeting will happen in May of this year, just two months away)

A positive result from that presentation could pave the way for more rapid uptake of the technology, and help EIQ integrate its tech quickly throughout the lucrative US healthcare market.

Remembering of course, that this is software which can be remotely activated by EIQ on existing US hospital IT and echo machine systems.

So we see the potential for near-term revenue.

AND then rapid growth throughout the US healthcare market.

Taken together, the growing pipeline of hospital integrations and progress on reimbursement are crucial steps towards widespread adoption in the US healthcare system.

This brings us to our EIQ Big Bet:

Our EIQ ‘Big Bet’:

“EIQ re-rates to a >$1BN market cap on successful commercialisation of its heart disease detection technology and/or an acquisition at a multiple of our Initial Entry price”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is a lot of work to be done, many risks involved - just some of which we list in our EIQ Investment Memo. Success will require a significant amount of luck. There is no guarantee that our Big Bet will ever come true.

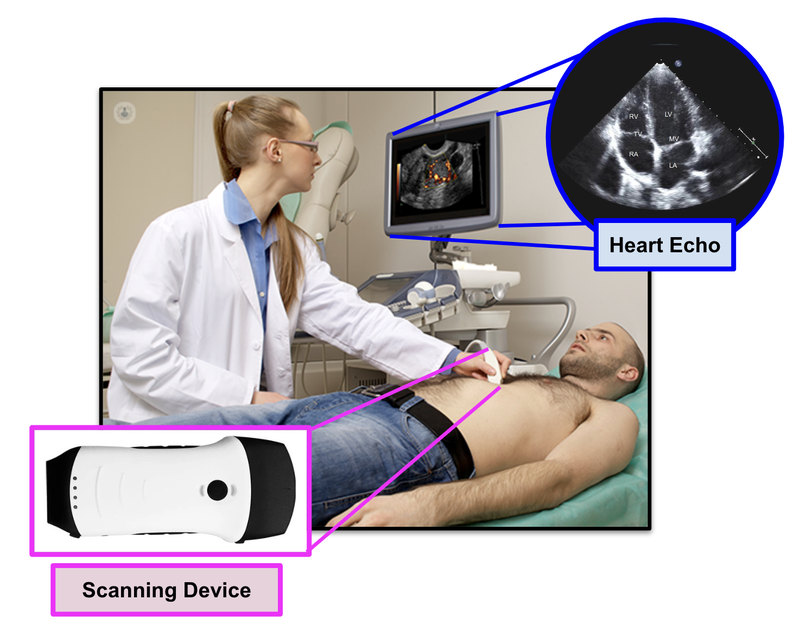

How does EIQ’s tech work?

EIQ’s product “EchoSolv” is a machine learning, AI-based decision support software that, when used together with a cardiologist, is able to detect heart diseases at a much better rate.

Cardiologists are specially trained doctors that are able to interpret heart conditions from 2D images that are presented from an ultrasound (known as an echo):

EIQ’s EchoSolv product can provide an actual 3D interpreted image of the heart, and provides assistance to the cardiologist in detecting heart related issues.

There are two key ways EIQ gets paid...

1. Reimbursement

Private insurance companies or public health programs will reimburse healthcare providers (like hospitals) that use EIQ’s product.

This is done through a reimbursement scheme of which EIQ receives a % of funds reimbursed.

Whenever EIQ’s product is used by a hospital the cost is not paid by the patient, but rather the health insurance pays the hospital and EIQ splits the revenue.

Think of this like a “sale”.

In order for EIQ to be eligible for payment it needed to:

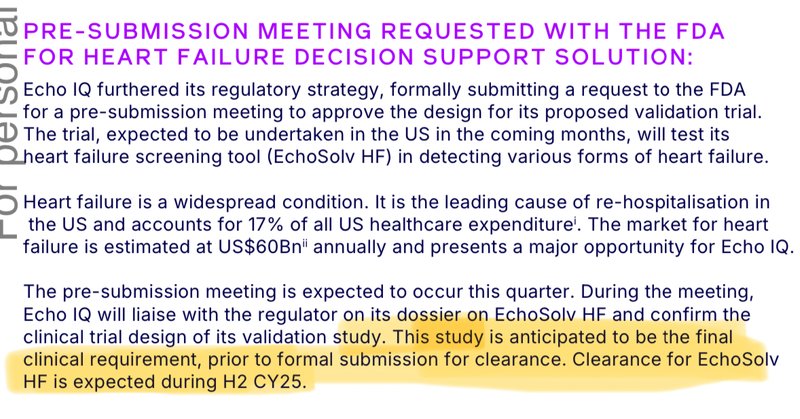

- secure FDA clearance (EIQ already has this for aortic stenosis, and is working on getting this for heart failure), and;

- a reimbursement code.

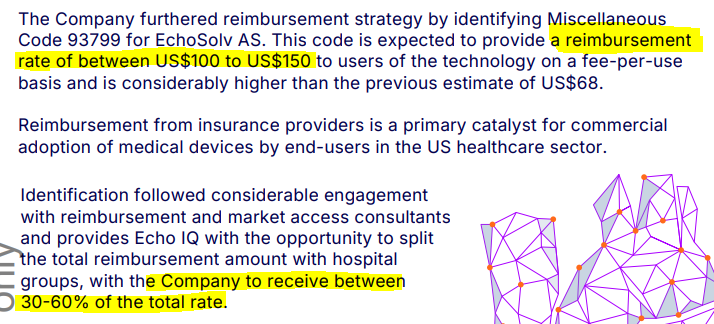

Last quarter EIQ identified a miscellaneous code for aortic stenosis reimbursement, which is expected to provide a reimbursement rate of between US$100 to US$150 to users on a fee-per-use basis.

This provides EIQ with the opportunity to split the total reimbursement amount with hospital groups, with the company to receive between 30-60% of the total rate.

Armed with FDA clearance and a reimbursement code, for sales to grow EIQ just needs more hospitals using its tech.

2. Licensing

EIQ’s second commercialisation strategy is to secure licensing partnerships with various organisations that provide services to patients with heart issues.

Organisations like medical device manufacturers and big pharma companies.

The type of companies we think would be most interested in EIQ’s tech are the ones that rely on diagnosis to be able to treat heart diseases - as we covered above.

EIQ’s tech is built around improving heart disease detection and diagnosis rates - so using EIQ’s tech means more patients are identified with conditions that require treatment.

More people that require treatment = more revenues for the organisations treating those patients.

On that note, let’s take a deeper look at the key updates that EIQ announced this week...

EIQ product is now being used in a top tier hospital

What happened?

EIQ’s EchoSolve product for aortic stenosis has been integrated in and is being used by cardiologists at the Beth Israel Deaconess Medical Centre.

What is our take?

The Beth Israel Deaconess Medical Centre is part of a network of hospitals linked in with Harvard University.

It is an extremely prestigious institution and operates as a flagship customer for EIQ.

There are also 30,000 echocardiograms done each year at the hospital.

Because EIQ has secured a reimbursement code, it means it will be paid for each time its technology is used.

The amount? US$100 to $150 per echo.

Back of the napkin calculations on the Beth Israel Deaconess Medical Centre number of echoes comes to:

30,000 x ~US$125 (at 80% utilisation rate) = US$3M (AUD$4.75M) annually.

Of that amount, EIQ would “expect to receive” between 30-60%.

(Source)

And this is just from one hospital network, EIQ has multiple hospital networks in its pipeline...

EIQ’s sales pipeline into the US hospital networks is strong

What happened?

EIQ announced that it is in advanced discussions with “multiple larger, multi-site hospital groups”.

In addition, EIQ has a pipeline of 60 individual sites that are preparing to use EIQ’s technology.

What is our take?

EIQ is using a well established adoption method... “try before you buy”.

For EIQ, building up its pipeline of hospitals is mostly about making it easy for cardiologists to use the product.

Remember, it is the insurance company that pays... not the hospital.

In addition to Beth Israel, EIQ has integration underway with at least four additional sites who have begun a “free trial period”.

The hassle of integrating a new system is one of the biggest barriers for uptake.

Which is why EIQ has appointed a new Chief Technology Officer to streamline this process.

EIQ secures new CTO to support growing integration demand

What happened?

EIQ has strengthened its management team with the appointment of Sam Dribin as a US-based CTO.

What is our take?

Sam has a very strong resume with nine years at CureMetrix where he most recently held the CTO position.

CureMetrix also sells an AI-based product that helps detect breast cancer from radiograms.

(this is a very similar product to EIQ, but a different disease).

We think that Sam’s experience in dealing with hospitals in the US and the challenges of integrating into large legacy systems is extremely compatible with EIQ’s current needs.

But it is not just hospitals that EIQ will be selling into, EIQ has also made progress on the “licensing front” of its product.

EIQ has started a fully funded trial with medical device company

What happened?

EIQ announced that it has commenced a “fully funded” medical device pilot trial with a leading global structural heart innovation company.

The trial is set to run through to 2025 and focus on quality assurance and patient recall.

What is our take?

This trial is a big step for EIQ towards securing a commercial licensing deal with a third party provider.

What kind of third party would be interested in EIQ’s technology?

Well, as we covered higher up in the note, we went down a bit of a rabbit warren here in an effort to answer the question for ourselves.

A quick Google search for “leading global structural heart innovation company” comes up with $42BN capped Edward Lifesciences.

(Of course, EIQ did not identify their partner and the commentary below is complete speculation on our part)

To get a sense of the potential value of EIQ’s technology, Edward Lifesciences recently acquired two companies for a combined US$1.2BN (contingent on FDA approvals - one of which was JenaValve Technology).

JenaValve is currently developing a TAVR (transcatheter aortic valve replacement) therapeutic product, which it expects to receive FDA approval for in 2025.

(TAVR is one of the procedures that may be needed in patients diagnosed with aortic stenosis)

(Source)

So, Edwards is paying billions for a medical device that can treat aortic stenosis.

It makes perfect sense why a company like this could be interested in EIQ’s technology.

EIQ’s technology can help detect aortic stenosis more accurately than “human only” assessments, which means a company with a therapeutic product could treat more patients (increasing its addressable market).

AND potentially open up a whole new segment of previously undetected and undiagnosed heart disease patients that will benefit from Edward Lifesciences’ product to get better - creating a big jump in "diagnostic yield".

(EIQ has already demonstrated that with its tech it can produce a 72% increase in detection vs human-only diagnosis for severe aortic stenosis).

The second part of that US$1.2BN deal was the Endotronix acquisition, where Edwards is looking to expand its Heart Failure therapeutic business.

(Source)

REMINDER: EIQ is working on AI tech that could enhance Heart Failure diagnosis rates too.

FDA clearance for EIQ’s Heart Failure tech is expected later this year... and that market opportunity is ~10x bigger than aortic stenosis for EIQ.

(another reason why an EIQ might be interesting to an Edwards Life Sciences)

(Source)

Now it’s important to note that Edward Lifesciences may not be the company EIQ is doing the trial with.

There are lots of device manufacturers that could fall into this category.

But we think that the story demonstrates the market for products within the aortic stenosis space, and the opportunity for EIQ to sell into the medical device segment.

EIQ’s reimbursement strategy is progressing

What happened?

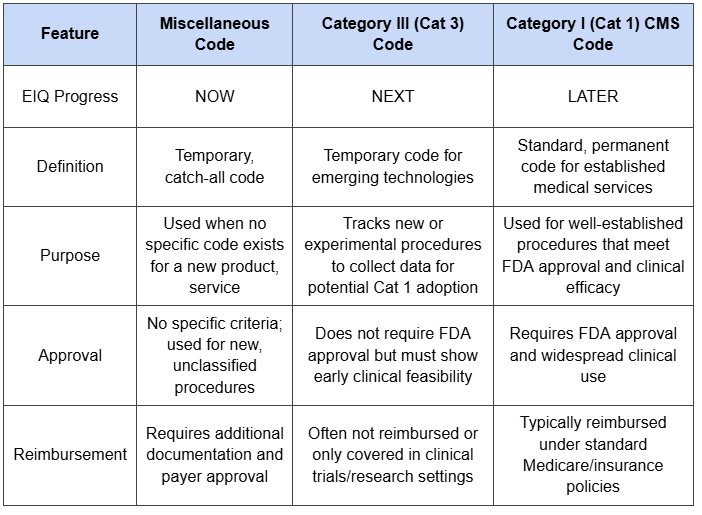

EIQ announced that it had set a date with the CMS review board for May 2025 to advance discussions on securing a Category III reimbursement code.

What is our take?

Last year, EIQ secured a miscellaneous reimbursement code for its EchoSolve product.

This was a big milestone for the company and meant that it could start to earn revenues whenever the product was used in a hospital.

The reimbursement amount was between US$100-$150 (which was higher than the anticipated US$64).

Securing a miscellaneous code is good... but the real goal is to get a Category I code.

A “Category I” code is used for well established medical services.

The reimbursement process under a Category I code is very straightforward and will catapult EIQ’s revenue potential.

In order to secure the Category I code, it will need to get a Category III code and prove that the EcoSolve product is “well established”.

(it’s a bit complicated)

EIQ can still earn revenue from its miscellaneous code, but Category I is what EIQ is really chasing.

EIQ says that it will likely secure Category III by the end of this year.

Passive buying tailwinds for an EIQ re-rate?

One thing we think the market may have overlooked with EIQ is this announcement on the 6th of December last year.

(Source)

EIQ became the most recent entrant into an index in our Portfolio.

For anyone new to markets - an index is just a collection of stocks that are big and liquid enough to be owned by a passively managed investment mandate.

Indexes are what the big fund managers use to evaluate their relative performance against.

That means these fund managers are forced to either own whatever gets into an index OR at the very least watchlist those companies and make a decision later.

The major outcome from this is some on market buying from funds for new entrants.

Why does this matter for EIQ?

Two of our best ever performers made it into indexes on their way to being multi-baggers:

Vulcan Energy Resources (ASX: VUL) - went from our Initial Entry Price of 20c to an all time high of $16.65.

Here is where Vulcan got included in the S&P all ordinaries index:

(Source)

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

Latin Resources (ASX: LRS) - went from our Initial Entry Price of 1.8c to a high of ~42c. Here is where Latin Resources got included in the S&P All Ordinaries index:

(Source)

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

Both of those companies started their runs to their highs off the back of index inclusion.

Of course it's worth pointing out that it wasn't index inclusion alone that sparked those second rallies.

Both Vulcan and Latin had sky high lithium prices and strong project level newsflow that would have worked in tandem with the index inclusion funds rolling into the stock.

Here is where EIQ comes into play...

EIQ recently got FDA clearance for its AI heart disease detection software for aortic stenosis (a common heart valve problem).

It is also working on FDA clearance for a similar product for heart failure, which has an even larger addressable market.

64 million people suffer from heart failure each year across the world, and the total cost of heart failure to the US health system is US$60BN a year.

With FDA clearance secured, commercialisation underway, and the heart failure product clearance to come, EIQ got included in the S&P/ASX All Tech index late last year....

(Source)

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

Lets see what EIQ can achieve in 2025...

We also have some strong catalysts to look forward to:

- FDA clearance for the Heart Failure product could be big for EIQ - that market could potentially be a 10x bigger opportunity for EIQ than its current approved aortic stenosis Product.

- Commercialisation on the aortic stenosis product could surprise to the upside too... any big sales deals could trigger a run too.

- A potential licensing deal with a major therapeutics company?

Any of these, we think, could trigger a rally in EIQ’s share price.

IF the share price starts running, fund managers will have a decision to make too - either buy EIQ and get some outperformance relative to the index, OR sit it out and risk underperforming...

We are hoping that on a net basis, it means more capital flows into EIQ which adds to the rally in the company’s share price.

Remember we said funds are currently forced to (at the very least) watchlist EIQ...

Ultimately, we want to see EIQ achieve our Big Bet which is as follows:

What’s next for EIQ?

🔄 Strategic partnership updates - we want to see EIQ advance discussions in this area to help rapidly roll out the company’s tech, grow EIQ’s revenue and build market share.

🔄 Australia and NZ pilot program - this program is with a ”leading global structural heart innovation company” - this will advance EIQ’s licensing revenue pathway and be a “proof of concept” study that EIQ can take into the US. We haven’t talked about this sales strategy much today, but you can read about it here Is FDA approval imminent for EIQ? What happens after that?

🔄 Heart Failure validation study with US based Group - the indication from EIQ’s most recent webinar is that the US based group is the prestigious Mayo Clinic, we think that the outcome of this study could be a big coup for EIQ.

🔲 Partnership with European re-seller to broaden market exposure - we want to see EIQ expand into new markets like Europe, in a previous webinar EIQ said the company was pursuing this opportunity.

🔲 CE Mark and TGA applications - this is so that EIQ can sell into Europe and Australia.

Next Thursday, 13th March, EIQ’s CEO will provide a progress update on the US commercialisation strategy for EchoSolv-AS over the first two months of CY2025, along with an outlook on the Company’s clinical development pipeline and other opportunities.

Click here to register for EIQ’s Webinar

What could go wrong?

At this stage of EIQ’s journey a key risk for the company is sales risk.

Today’s news de-risks this slightly, but we are conscious of the reimbursement process being relatively technical.

For EIQ’s tech to be widely adopted it will need to have access to the far more streamlined reimbursement process.

At the moment, EIQ is having to do a lot of educating for its integration partners which is expected this early into commercialisation, but we are conscious that this may cause revenue growth to be slower than expected in the short term.

Sales/Commercialisation risk

EIQ is reliant on its partners, both under the licensing and reimbursement strategy, to use EIQ’s product. If EIQ’s product is not used (because it doesn’t add value back to the provider), then it won’t be able to generate revenue. There is no guarantee that EIQ’s product will be used by its partners and, therefore, no guarantee of revenue.

Source: “What could go wrong” - EIQ Investment Memo 6 Sept 2024

There is also an element of “regulatory risk” as well.

EIQ has a second product being developed for heart failure.

There is no guarantee that the product receives FDA clearance which would impact the company’s future growth prospects.

There is also no guarantee that EIQ receives any further approvals with its application for “full category III CPT code”. This could slow down adoption from potential users of EIQ’s tech.

Regulatory Risk

EIQ has applied for FDA clearance under the 510(k) pathway for aortic stenosis and will apply for FDA clearance for heart failure. There is no guarantee that the FDA will provide clearance, and the application may be rejected. Also, EIQ’s strategy is reliant on securing reimbursement for its product. If EIQ is not able to secure a reimbursement deal then its commercialisation strategy may need to pivot.

Source: “What could go wrong” - EIQ Investment Memo 6 Sept 2024

Another risk is “funding and dilution risk”.

EIQ is a small cap which is essentially pre-revenue (it did $200k of revenue last half).

EIQ had $5.3M cash in the bank at 31 December 2024 and then received $1.2M from an R&D tax refund in February.

It's possible that sales of its technology don't arrive as quickly as the market expects.

In that scenario EIQ may need to tap markets for cash to fund the business & develop its heart failure technology, including validation trials or anything else requested by the FDA.

Funding and dilution risk

EIQ is a small cap company and is essentially pre-revenue. This means that EIQ may need to raise funds in the future via capital raises that may incur dilution to shareholders.

Source: “What could go wrong” - EIQ Investment Memo 6 Sept 2024

Our EIQ Investment Memo:

In our EIQ Investment Memo, you can find the following:

- What does EIQ do?

- The macro theme for EIQ

- Our EIQ Big Bet

- What we want to see EIQ achieve

- Why we are Invested in EIQ

- The key risks to our Investment Thesis

- Our Investment Plan

General Information Only

S3 Consortium Pty Ltd (S3, ‘we’, ‘us’, ‘our’) (CAR No. 433913) is a corporate authorised representative of LeMessurier Securities Pty Ltd (AFSL No. 296877). The information contained in this article is general information and is for informational purposes only. Any advice is general advice only. Any advice contained in this article does not constitute personal advice and S3 has not taken into consideration your personal objectives, financial situation or needs. Please seek your own independent professional advice before making any financial investment decision. Those persons acting upon information contained in this article do so entirely at their own risk.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.